- Strong consumer demand for Ontex products drove outstanding top-line outperformance across all 3 categories

- Resilient Adjusted EBITDA margins for the Group excluding Ontex Brazil, where actions are being taken to restore profitability

- Significant benefit to earnings and cash flow from refinancing and lower tax rate

Aalst-Erembodegem, March 6, 2018 – Ontex Group NV (Euronext Brussels: ONTEX; ‘Ontex,’ ‘the Group’ or ‘the Company’) today announced its results for the twelve months ending December 31, 2017.

2017 Highlights

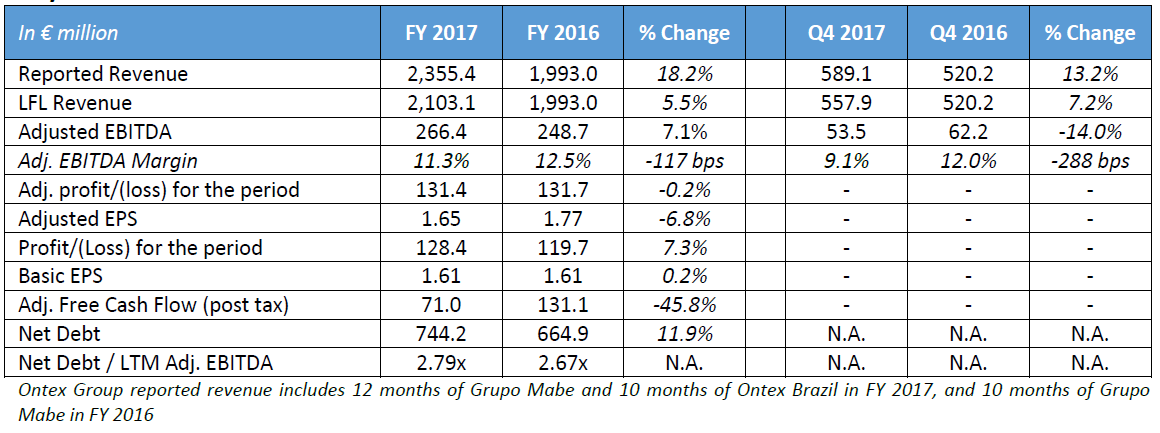

- Strong demand for our products, with revenue of €2.36 billion, up 18.2% on a reported basis

- 5.5% like-for-like (LFL), including very strong Mature Market Retail LFL of 5.1%

- Adjusted EBITDA of €266.4 million was 7.1% higher yoy, despite a €7.8 million FX headwind

- Group Adjusted EBITDA margin of 11.3% included a resilient performance outside of Brazil of 12.0%

- Ontex Brazil, acquired in March 2017, had an adjusted EBITDA margin of 3.8% which was highly impacted by an exceptional €15 million charge in December 2017

- Adjusted earnings per share of €1.65, down 6.8% compared to a year ago

- Debt refinancing to deliver estimated annual savings before tax of €10 million from 2018 and longer maturities with interest rate risk largely hedged

- The Board of Directors proposes to pay a gross dividend of €0.60 per share, an increase of €0.05 per share subject to approval by shareholders at the next general meeting

Key Financials FY 2017 and Q4 2017

Charles Bouaziz, Ontex CEO: “Our teams delivered strong LFL revenue in 2017, ahead of our markets despite very competitive conditions. This growth is across all 3 categories, and we gained share in most of our markets, including our leading position in European retailer brands. Our efforts to drive this strong revenue growth to adjusted EBITDA largely mitigated significant input cost and FX headwinds and capacity constraints. However, the Brazilian business acquired last year impacted overall group profitability. While disappointing, we have taken appropriate actions and will continue to do so, and remain confident in the long-term opportunity for Ontex from this foothold in a major personal hygiene market. Going forward, we will have significant recurring benefits to earnings and cash flows from a successful debt refinancing and lower tax rate. We expect 2018 to be a year of further progress consistent with our ambition of being a leading international consumer goods company.”

Market Dynamics

The Babycare, Femcare and Adult Inco categories in markets where we are present were estimated to be broadly stable in 2017 compared to a year ago. The Babycare category experienced strong price pressure throughout 2017, led by international brands’ promotional activities. At the same time, baby pants grew strongly in Europe, whereas diaper sales declined. The Adult Inco category was the highest growing category in 2017.

Retailer brands continued to grow faster than the overall market in Europe, where volumes sold of retailer brand babycare products (diapers and pants) exceeded 50% of the total babycare category. These trends reflect the increasing number of consumers who choose for retailer brands based on their attractive combination of performance and value.

Market prices for all our main commodity raw materials were higher in 2017 than in 2016, and while an increase had been anticipated, particularly for oil-based raw materials, actual 2017 raw material indices were above our initial expectations.

Several currencies in which we do business weakened versus the euro in 2017, such as the Brazilian Real, British Pound, Mexican Peso and Turkish Lira, while the Russian Rouble strengthened.

Overview of Ontex Performance in 2017

We saw a strong performance in our underlying business in 2017 and a disappointing first year from the Brazilian business acquired in March 2017.

On a LFL basis, the underlying Ontex business continued to perform well. Ontex Group excluding the Brazilian acquisition, representing more than 90% of FY 2017 revenue of €2.36 billion, significantly outperformed consumer staples in a broadly flat personal hygiene market, delivering 5.5% LFL revenue growth across all three categories. This demonstrated strong consumer demand for the portfolio of Ontex products, resulting in market share gains across most of our Divisions. Our Mature Market Retail had a particularly strong performance, and confirmed the strengths we have built over decades in these markets after some temporary challenges faced in 2016.

Adjusted EBITDA margins of the Group excluding Brazil proved robust at 12.0% compared to 12.5% in 2016. This was a resilient performance, with our cost savings and efficiencies programs largely offsetting significant external headwinds, and some capacity constraints that limited our profitability in the near term.

The overall performance of the Brazilian business acquired in March 2017 fell well short of our expectations. Challenging market conditions provided a difficult backdrop. At the end of the year, we learned that discounts to customers, a standard retail industry practice, had been made above the budgeted levels, and that these excess discounts had not been registered during the year. As a consequence, in December, we took a charge of €15 million to revenue and adjusted EBITDA to fully cover the year, resulting in the 2017 adjusted EBITDA margin in Brazil of 3.8%.

Significant actions have already been taken to address the issues in Brazil, including some changes in the sales incentive system and reinforced processes and controls. We are reviewing ways in which we can sustainably improve the business performance on the top and bottom line.

Despite these challenges, we remain confident in the long-term value of the Brazilian business to the Ontex Group. It provides an important branded position in the 4th largest hygiene market in the world, with opportunities to improve manufacturing efficiencies and leverage our innovation expertise as originally foreseen.

OUTLOOK

We have three priorities for 2018:

- continue investing in initiatives which will support sustainable profitable growth

- strengthen further the underlying Ontex business, continuing to build on our leadership position in retailer brands in Europe and on our portfolio of local brands

- achieve sustainable improvements in our Brazil business

In challenging markets, we expect a better balance between top line and profitability in 2018. On the top line, we expect a low single-digit LFL revenue growth in broadly flat hygiene markets. After a lower first half of the year, we anticipate a sequential improvement in adjusted EBITDA margins in the second half, as our actions across all aspects of the business, including pricing, mix and cost savings, increasingly take effect. Our commitment to improve our margins over time is unchanged. We will work through the short-term challenges we are facing, while our long-term objectives remain fully intact.

Operation review: Categories

Babycare

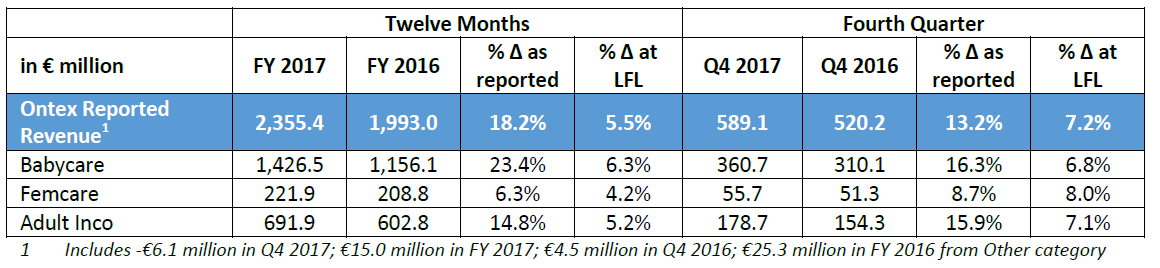

FY 2017 category revenue for Babycare increased 23.4% on a reported basis, and 6.3% on a LFL basis. Our local brands outperformed underlying category growth in the majority of our markets, while our LFL revenue for retailer brands in the MMR Division grew significantly ahead of their markets. Sales of baby pants were again strongly higher.

Femcare

Femcare category revenue in FY 2017 was up 6.3% as reported and 4.2% higher on a LFL basis. We gained new business by supporting leading retailers with their own brands in Western Europe, and grew ahead of the overall category.

Adult Inco

Revenue in the Adult Inco category grew 14.8% on a reported basis, and was up 5.2% on a LFL basis in 2017. LFL revenue growth was driven by 10% higher sales in retail channels, where we have a number of leading positions, while sales in institutional channels also rose. Sales of adult pull-ups continued to experience faster growth.

Operation review: Divisions

Mature Market Retail

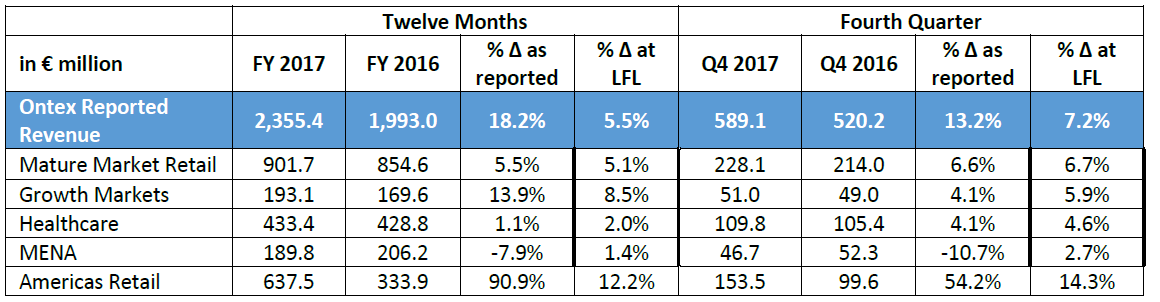

FY 2017 revenue in the Mature Market Retail Division grew 5.1% versus last year, significantly ahead of underlying market growth. In a highly competitive environment, our volume-led revenue growth across all 3 categories was due to new business as well as our ongoing customers growing their business. This revenue performance is the result of our relentless focus on supporting retail customers with innovative products and services, enabling them to compete successfully with international brands. We continued to invest in innovation, shopper understanding and supply of faster-growing, higher-margin products, which should underpin our business in the coming year.

Growth Markets

In a very competitive environment, the Growth Markets Division recorded 8.5% higher revenue in FY 2017, outpacing local markets. This is a strong performance from a larger base business after three years of double-digit revenue growth, which confirms our model of driving both retailer brands and our own brands. In order to support further profitable growth in this Division and meet local consumer demands, we continued to invest in production, opening our first production site in Sub-Saharan Africa (Ethiopia) and increasing capacity in our Russian plant.

Healthcare

Healthcare Divisional revenue was up 2.0% for FY 2017, outperforming estimated market growth. The revenue increase was due to higher volumes of our brands, for example in pull-ups, a convenient and discreet product which has enjoyed good growth. We also continued to evolve our business model, by taking account of the growing consumer need for performance, dignity and comfort. This will allow us to enhance our offer of high-quality products at affordable prices through existing and emerging market channels.

MENA

Middle East and North Africa Divisional revenue was up 1.4% in FY 2017 after double-digit growth in 2016. The limited revenue growth in 2017 was primarily due to very competitive conditions in Turkey Babycare, in which low-price products grew at the expense of the leading brands, such as our Canbebe diapers. At the same time, we maintained our leading position in Adult Incontinence, and grew Babycare volumes in most of our other markets.

Americas Retail

Revenue in our Americas Retail Division grew strongly, up 12.2% in FY 2017. In Mexico, our Babycare and Adult Inco businesses had solid volume growth ahead of their categories, thanks to strong consumer demand for our portfolio of local brands. Sales in the USA were also higher than the previous year. Following completion of the acquisition in March 2017, Ontex Brazil contributed 10 months to 2017 reported revenue. Compared to the same period in 2016 under previous ownership, sales in the Babycare category were lower amid highly competitive conditions including a decline in the category, while the Adult Inco category increased and we strengthened our position as the leading brand in the country.

Operational review: geographies

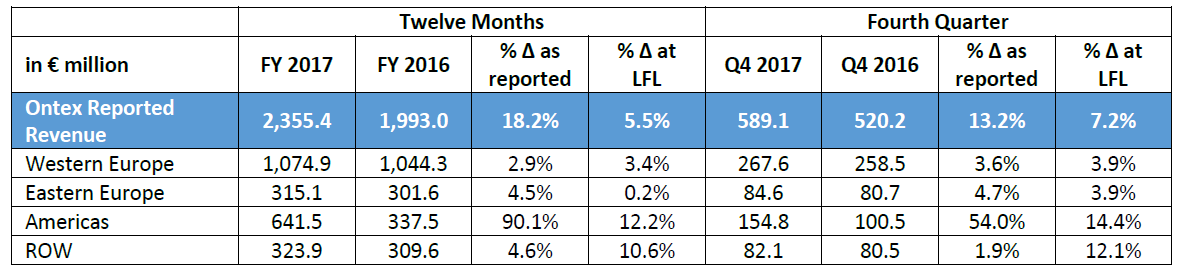

FY 2017 revenue was broad-based with most geographies delivering higher LFL revenue. As a result of double-digit LFL growth and our Brazil acquisition, sales in the Americas rose to 27% of Group sales, while the proportion of Group sales in Western Europe was less than 50% for the first time ever, despite the solid increase in this region.

FINANCIAL REVIEW

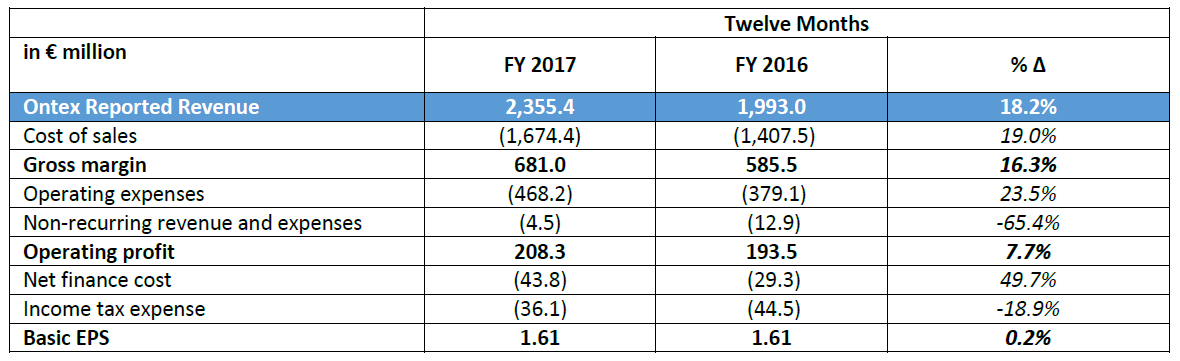

Selected P&L Financial Information

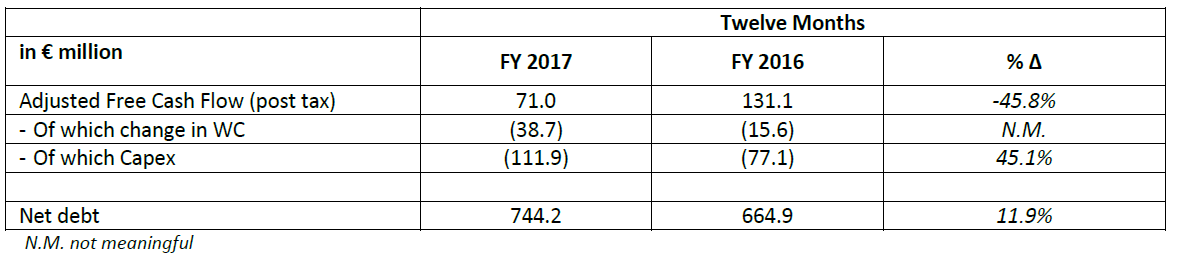

Selected Liquidity Financial Information

Gross Margin

2017 gross margin was €681.0 million, an increase of 16.3% compared to last year. Gross margin as a percentage of sales was 47 basis points lower, from 29.4% in 2016 to 28.9% in 2017. Strong LFL revenue growth and savings generated throughout the year did not fully compensate higher raw material pricing, and to a lesser extent a negative FX impact and additional manufacturing expenses to service the top line.

Adjusted EBITDA

2017 adjusted EBITDA was 7.1% higher than in 2016 at €266.4 million. Other than the evolution in gross margin as detailed above, we absorbed the temporary impact of higher distribution expenses mainly due to strong revenue growth, and continued to invest in our sales and marketing capabilities.

Foreign Exchange

Movements in the value of foreign currencies versus the euro had a negative impact on Group revenue and Adjusted EBITDA in 2017. The full year impact of -€21.3 million on revenue was mainly related to a weakening of the Turkish Lira and the British Pound, the Mexican Peso and US Dollar, while the Russian Rouble and the Polish Zloty strengthened compared to the previous year.

The FX impact on Adjusted EBITDA in 2017 was -€7.8 million, mostly from a weakening of the British Pound and the Turkish Lira, while the Russian Rouble and the Czech Koruna were stronger.

In addition to the above, the Brazilian Real weakened in 2017 versus the exchange rate at the time of acquisition.

Net Finance Costs

In 2017 net finance costs were €43.8 million. Compared to 2016, the increase in net finance costs is fully explained by higher net exchange rate differences related to financing activities. Total interest expenses in 2017 were above a year ago, and were essentially offset by the gain arising from the amendment of our syndicated loan.

Income Tax Expense

The income tax expense was €36.1 million for 2017, resulting in an effective tax rate of 22.0%, below our guidance of approximately 24%.

Working Capital

Working capital as a percentage of revenue was 11.3% in 2017, within our objective of keeping working capital requirements at or below 12% of revenue.

Capex

Capital expenditures were €111.9 million in 2017, or 4.8% of revenue. This is above our historical level of investment as expected and previously disclosed, mainly reflecting the capex program foreseen in the acquisition of Ontex Brazil, and to a lesser extent increasing capacity of faster growing, margin-accretive products. We expect this to have a positive impact on our manufacturing and supply chain as the new production comes online, alleviating the temporary pressures we have absorbed from strong revenue growth.

Adjusted Free Cash Flow (post tax)

Adjusted free cash flow (post tax) was €71.0 million in 2017, 45.8% lower than in 2016. The main reasons for the decline are higher capex as planned, increased working capital and cash taxes paid. The higher working capital was due to the significant build-up of working capital in Ontex Brazil. The carved-out company, which became operational in January 2017, did not receive historical receivables from Hypermarcas. This effect was fully expected and was factored into the cash consideration. Excluding this one-time impact, adjusted free cash flow (post tax) would have been some 15% lower than in 2016.

Financing

Net debt at December 31, 2017 amounted to €744.2 million, and net leverage based on the last twelve months Adjusted EBITDA was 2.79x.

The refinancing of debt in the second half of 2017 resulted in a meaningful extension of debt maturities to 2022 and 2024, and a lower average cost of debt with the interest rate risk largely hedged, in line with the Group’s hedging policy. Estimated annual savings before tax are expected to be approximately €10 million.

Dividends

The Board of Directors has proposed a dividend of €0.60 per share, an increase of €0.05 per share subject to shareholder approval at the next Annual General Meeting of Shareholders.

Corporate information

The above press release and related financial information of Ontex Group NV for the twelve months ended December 31, 2017 was authorized for issue in accordance with a resolution of the Board on March 5, 2018.

CONFERENCE CALL

Management will host a presentation for investors and analysts on March 6, 2018 at 8:00am GMT/9:00am CET.

A copy of the presentation slides will be available at http://www.ontexglobal.com/

If you would like to participate in the conference call, please dial-in 5 to 10 minutes prior using the details below:

United Kingdom +44 (0)330 336 9105

United States +1 646 828 8156

Belgium +32 (0)2 404 0659

France +33 (0)1 76 77 22 74

Germany +49 (0)69 2222 13420

Passcode: 6390577

FINANCIAL CALENDAR 2018

Q1 2018 May 9, 2018

AGM May 25, 2018

H1 2018 July 26, 2018

Q3 2018 November 7, 2018

Contact

Notes to the Consolidated Financial Information

Note 1 Legal Status

Ontex Group NV is a limited-liability company incorporated as a “naamloze vennootschap“ (“NV”) under Belgian law with company registration number 0550.880.915. Ontex Group NV has its registered office at Korte Keppestraat 21, 9320 Erembodegem (Aalst), Belgium. The shares of Ontex Group NV are listed on the regulated market of Euronext Brussels.

Note 2 Accounting Policies

The accounting policies used to prepare the financial statements for the period from January 1, 2017 to December 31, 2017 are consistent with those applied in the audited consolidated financial statement for the year ended December 31, 2016 of Ontex Group NV. The accounting policies have been consistently applied to all the periods presented.

Note 3 Events after the Reporting Period

No events

Note 4 Auditors Report

The statutory auditor has confirmed that the audit, which is substantially complete, has not to date revealed any material misstatement in the draft consolidated accounts, and that the accounting data reported in the press release is consistent, in all material respects, with the draft accounts from which it has been derived.

Note 5 Alternative Performance Measures

Alternative performance measures (non-GAAP) are used in this press release since management believes that they are widely used by certain investors, securities analysts and other interested parties as supplemental measure of performance and liquidity. The alternative performance measures may not be comparable to similarly titled measures of other companies and have limitations as analytical tools and should not be considered in isolation or as a substitute for analysis of our operating results, our performance or our liquidity under IFRS.

Like-for-like revenue (LFL)

Like-for-like revenue is defined as revenue at constant currency excluding change in scope of consolidation or M&A.

Non-recurring Income and expenses

Items classified under the heading non-recurring income and expenses are those items that are considered by management not to relate to items in the ordinary course of activities of the Company. They are presented separately as they are important for the understanding of users of the consolidated financial statements of the “normal” performance of the company due to their size or nature. The non-recurring income and expenses relate to:

- acquisition-related expenses;

- changes to the measurement of contingent considerations in the context of business combinations;

- business restructuring costs, including costs relate to the liquidation of subsidiaries and the closure, opening or relocations of factories;

- impairment of assets.

Non-recurring income and expenses of the Group are composed of the following items presented in the consolidated income statement:

- Income/(expenses) related to changes to Group structure; and

- Income/(expenses) related to impairments and major litigations.

EBITDA and Adjusted EBITDA and related margins

EBITDA is defined as earnings before net finance cost, income taxes, depreciations and amortizations. Adjusted EBITDA is defined as EBITDA plus non-recurring income and expenses and excluding non-recurring impairment of assets. EBITDA and Adjusted EBITDA margins are EBITDA and Adjusted EBITDA divided by revenue.

Net financial debt/LTM Adjusted EBITDA ratio (Leverage)

Net financial debt is calculated by adding short-term and long-term debt and deducting cash and cash equivalents. LTM adjusted EBITDA is defined as EBITDA plus non-recurring income and expenses and excluding non-recurring impairment of assets for the last twelve months (LTM).

Adjusted Free Cash Flow

Adjusted Free Cash Flow is defined as Adjusted EBITDA less capital expenditures (Capex, defined as purchases of property, plant and equipment and intangible assets), less change in working capital, less income taxes paid.

Adjusted Profit & Adjusted EPS (earnings per share)

Adjusted Profit is defined as profit for the period plus non-recurring income and expenses and tax effect on non-recurring income and expenses, attributable to the owners of the parent. Adjusted EPS is Adjusted Profit divided by the weighted average number of ordinary shares.

Working Capital

The components of our working capital are inventories plus trade receivables and prepaid expenses and other receivables plus trade payables and accrued expenses and other payables.

See appendices in the above press release.

DISCLAIMER

This report may include forward-looking statements. Forward-looking statements are statements regarding or based upon our management’s current intentions, beliefs or expectations relating to, among other things, Ontex’s future results of operations, financial condition, liquidity, prospects, growth, strategies or developments in the industry in which we operate. By their nature, forward-looking statements are subject to risks, uncertainties and assumptions that could cause actual results or future events to differ materially from those expressed or implied thereby. These risks, uncertainties and assumptions could adversely affect the outcome and financial effects of the plans and events described herein.

Forward-looking statements contained in this report regarding trends or current activities should not be taken as a report that such trends or activities will continue in the future. We undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. You should not place undue reliance on any such forward-looking statements, which speak only as of the date of this report.

The information contained in this report is subject to change without notice. No re-report or warranty, express or implied, is made as to the fairness, accuracy, reasonableness or completeness of the information contained herein and no reliance should be placed on it.

In most of the tables of this report, amounts are shown in € million for reasons of transparency. This may give rise to rounding differences in the tables presented in the trading update.

This trading update has been prepared in Dutch and translated into English. In the case of discrepancies between the two versions, the Dutch version will prevail.